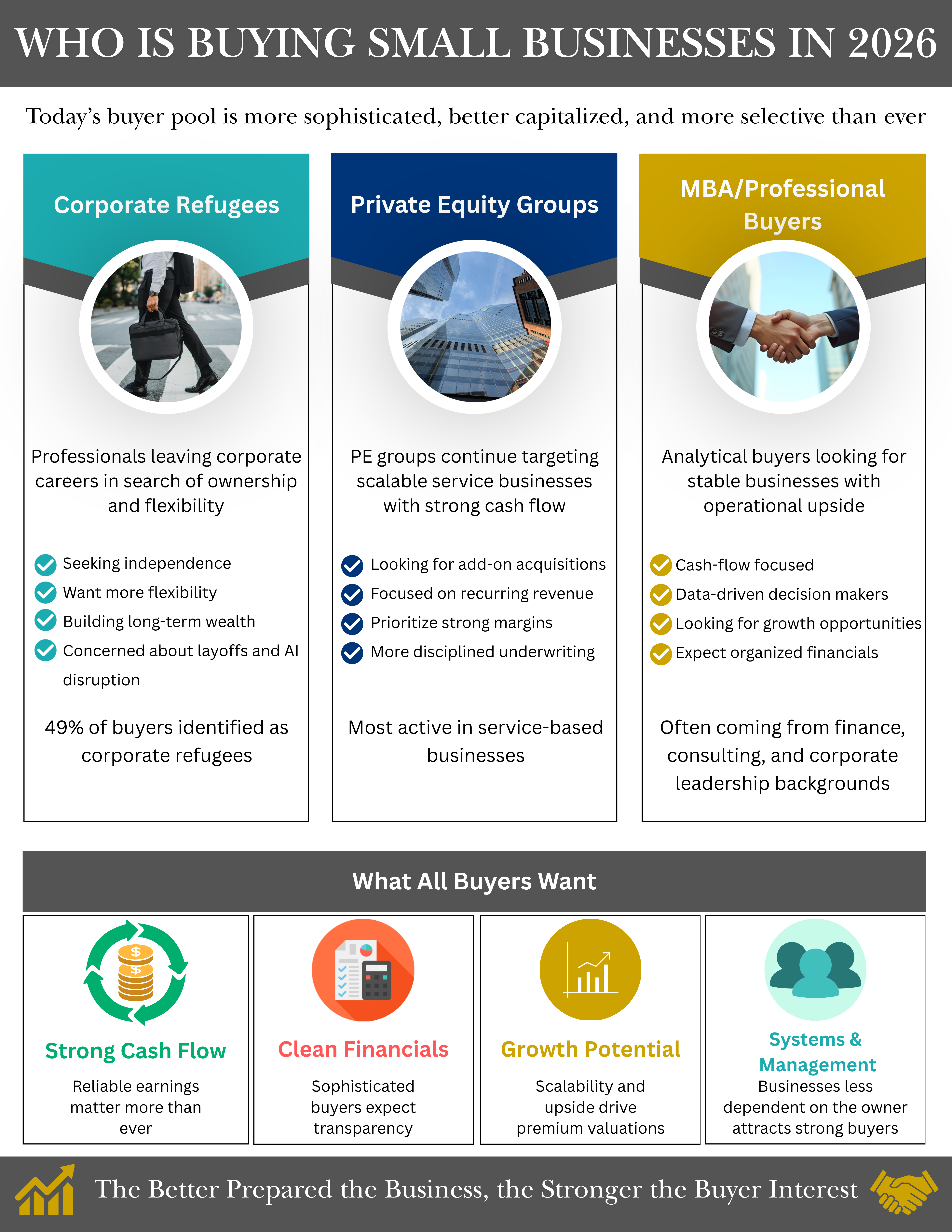

Who is Buying Small Businesses in 2026

As the small business buyer landscape continues to evolve, today’s buyers are more sophisticated, better capitalized, and more selective than ever before. While individual entrepreneurs remain active in the market, we are seeing increased participation from corporate professionals, private equity groups, and experienced business operators looking to acquire established companies.

Many buyers are leaving traditional corporate careers in pursuit of business ownership, financial independence, and greater flexibility. At the same time, private equity firms and professional buyers continue to target businesses with strong cash flow, scalable operations, and opportunities for growth.

As buyer expectations rise, businesses with clean financials, strong management teams, and clear growth potential are attracting the most interest. Owners considering a future sale should focus on preparing their business today to maximize value and appeal to today’s increasingly sophisticated buyer pool.

Corporate professionals, often referred to as “corporate refugees,” now represent a growing segment of the buyer market. Many are seeking greater control over their careers, additional income streams, or an alternative to the uncertainty of traditional employment. These buyers are often well-educated, financially stable, and willing to invest in businesses with a proven track record.

Private equity groups also remain active, particularly in service-based businesses with recurring revenue and strong profit margins. While these buyers continue to pursue acquisition opportunities, they have become increasingly disciplined in their evaluation process. Businesses with documented systems, reliable financial reporting, and expansion opportunities are often the most attractive acquisition targets.

Overall, regardless of the buyer type, the common factors that consistently drive interest are strong cash flow, transparent financial records, growth opportunities, and businesses that are not heavily dependent on the owner. As the market becomes more competitive and buyers become more selective, business owners who invest time in preparing their company for sale are often rewarded with stronger buyer interest, smoother transactions, and higher valuations.

Buying a Distressed Business: 4 Reasons Why It Can Work (and Why It’s Not for Everyone)

It’s no surprise within the business for sale market, most buyers walk away from struggling businesses. They see risk, uncertainty, and too many problems to fix.

But experienced buyers often see something else, they see opportunity.

A distressed business is not just a failing company. In many cases, it is a business with real assets, existing customers, and a place in the market, but one that has been poorly managed, neglected, or hit by temporary challenges.

That difference matters.

For the right buyer, buying a distressed business can be a chance to acquire something valuable at a lower price and improve it over time. But this approach requires more than optimism. It takes experience, clear thinking, and the financial ability to handle setbacks along the way.

This is not a beginner strategy. But for those who are prepared, it can be a powerful one.

1. Lower Purchase Price with Real Assets Already in Place

One of the biggest advantages of buying a distressed business is the price.

When a business is underperforming, owners are often motivated to sell. They may be dealing with financial pressure, burnout, or frustration after trying to fix ongoing issues. Because of this, the asking price is often lower than what the business could be worth if it were running properly.

What you are buying is not just current performance, but underlying value.

That value can include:

-Equipment and physical assets

-Existing customers or contracts

-Brand recognition in the local market

-A location that is already set up for operations

-Basic systems and processes, even if they need improvement

For many buyers, this can be more cost-effective than starting from scratch. Opening a new business often requires significant upfront investment before generating any revenue. In contrast, buying a distressed business may already have the foundation in place.

However, it is important to understand that a lower price does not mean a lower total investment. The purchase price is only part of the equation. You should also expect to invest time and money into fixing what is not working.

The real opportunity lies in the gap between what the business is today and what it could become with better execution.

2. Less Competition Creates Better Buying Conditions

In most markets, strong businesses attract the most attention. Buyers compete for companies with steady revenue, clean financials, and predictable performance. These deals often receive multiple offers, which can drive up prices and make it harder for buyers to stand out.

Distressed businesses tend to sit on the other side of that dynamic.

Because they come with uncertainty, many buyers choose to avoid them entirely. This naturally reduces competition. Fewer buyers means fewer bidding situations and less pressure to rush into a decision.

This can create a more favorable environment for thoughtful buyers.

With less competition, you may have:

-More time to review financials and operations

-Greater ability to ask questions and verify information

-More flexibility in negotiating terms

-A better chance of structuring a deal that works for both sides

In some cases, sellers are also more open to creative solutions, especially if they are eager to move on. This might include flexible payment terms or transition support.

That said, less competition does not automatically mean a good deal. The lack of interest from other buyers could be a sign that there are real issues to understand and address.

The advantage comes from being willing and able to evaluate those issues clearly, not from ignoring them.

3. You Are Stepping Into an Existing Business, Not Starting From Zero

Starting a business from scratch can be expensive, time-consuming, and uncertain. It can take months, or even years, to build customers, hire a team, and generate steady revenue. A distressed business is different because it is already operating.

Even if performance is weak, there is usually some level of activity in place. Most distressed businesses already have:

-Customers who are still buying

-Employees who understand day-to-day operations

-Supplier and vendor relationships

-A physical location or online presence

-Existing workflows (even if they need improvement)

This gives you a real starting point. Instead of building everything from zero, your focus shifts to improving what is already there.

In many cases, relatively small changes can make a noticeable impact, such as:

-Improving scheduling and staff efficiency

-Reducing waste or unnecessary expenses

-Tightening cost controls

-Adjusting pricing

– Improving customer service

However, it is important to be realistic. Not every business has a strong foundation. Some may have lost key customers, developed a damaged reputation, or accumulated internal and operational issues that take time to correct. The key is determining whether the business is something a buyer can build on or something that requires significant rebuilding.

This is where the real opportunity comes in. Many distressed businesses are not failing because there is no demand; they are struggling because of how they are being run. Issues such as poor marketing, inefficient operations, weak financial controls, inconsistent service or product quality, and lack of leadership are common. These are often fixable with the right approach.

For example, a business with an absentee owner may underperform simply because no one is paying close attention to daily operations. A hands-on owner can introduce structure, accountability, and consistency, which can lead to immediate improvements without changing the core business.

The goal is not to reinvent the business, but to clearly identify what is not working, focus on the highest-impact improvements, and strengthen execution step by step. Experience plays a critical role in this process. Knowing what to prioritize, how to manage people effectively, and how to make decisions under pressure can significantly influence the outcome. Without that experience, it is easy to spend time and resources on the wrong changes while the underlying problems remain unresolved.

4. Successful Turnarounds Can Lead to Significant Value Growth

When a distressed business is improved successfully, the increase in value can be meaningful.

A business that was once underperforming can become stable, profitable, and more attractive to future buyers. This creates several potential paths forward:

-Continue operating the business for steady income

-Sell the business at a higher valuation

-Expand by acquiring additional businesses

For some investors and operators, this is a repeatable strategy. They focus on identifying underperforming businesses, improving them over time, and then realizing the value they have created.

However, it is important to understand that this outcome is not guaranteed. Turnarounds take time, and results are not always predictable.

The value is created through consistent effort, disciplined decision-making, and the ability to adapt when things do not go as planned.

A Word of Caution: The Risks Are Real

While the potential benefits of buying a distressed business are clear, it is important to be direct about the risks involved. In most cases, this type of acquisition is not a good fit for first-time buyers. Although the lower purchase price can be appealing, distressed businesses are often more complex and difficult to fix than they initially appear. Instead of learning how to run a business step by step, the buyer is stepping into a situation where multiple problems must be addressed at the same time.

These challenges can include unstable or declining revenue, disorganized operations, employee turnover or low morale, loss of customers, or even a damaged reputation. In some cases, there may also be hidden liabilities or incomplete financial information, which can make it harder for the buyer to fully understand the true condition of the business. One of the most critical aspects of any turnaround is knowing what to fix first. If the buyer focuses on the wrong issues, time and resources can be wasted while the business continues to struggle.

Financial risk is another major factor to consider. Many distressed businesses require more capital than expected, and the buyer should be prepared for additional working capital needs, unexpected expenses, delays in reaching profitability, and even periods with little or no income. Without a financial cushion, even small setbacks can turn into serious problems.

There are situations where a distressed business can work for a first-time buyer, but they are less common. It may make sense if the buyer has strong experience in the industry, solid operational or problem-solving skills, access to additional capital, and support from experienced partners or advisors. Even in these cases, success depends on having a clear and realistic plan in place before completing the purchase.

Final Thoughts

Buying a distressed business is not about taking reckless risks. It is about understanding a situation clearly and making informed decisions.

These opportunities exist because most buyers choose to avoid them. That is what creates the potential for value, but it is also what creates the risk.

For experienced buyers with the right skills and financial resources, distressed businesses can offer a path to acquire undervalued assets and improve them over time.

For others, a more stable business may be a better starting point.

As with any business opportunity, the key is knowing where you stand, what you are capable of handling, and whether the opportunity in front of you truly makes sense.

Read More

Red Flags When Buying a Business: Why Due Diligence Matters

Red flags when buying a business are not always immediately obvious, but spotting them early is essential to making a smart purchase. Buying an existing business can be one of the fastest ways to step into ownership with an established brand, customer base, and cash flow.

However, even the best opportunities can have hidden problems. These issues can threaten long-term success. Without a careful due diligence process, buyers risk taking on financial, legal, or operational issues. These problems can quickly turn a good deal into a costly mistake.

Identifying potential red flags early protects your investment. It also gives you leverage to negotiate better terms or walk away before it’s too late. Here are some of the most common red flags every business buyer should watch for during a business sale.

Financial Statements: Key Warning Signs to Watch

One of the first places to look for red flags is in the financial statements. Numbers tell a story, and if that story doesn’t make sense, it’s often a sign of deeper issues. Missing or inconsistent financial records, like incomplete bookkeeping or unaudited statements, can show poor management. They may also suggest attempts to hide problems.

Falling revenue or smaller profit margins may show lost customers, market changes, or costly inefficiencies that need fixing. Likewise, unexplained expenses or erratic cash flow patterns are warning signs that deserve close scrutiny.

And while future projections can be helpful, they should be grounded in reality, not optimism. Before moving forward, it’s smart to have a qualified CPA check the company’s financials. This will ensure the numbers are correct.

Owner and Client Dependence: Risks of Over-Reliance

Another major red flag to watch for is a business that’s overly dependent on the current owner or a handful of key clients. When the owner handles customer relationships and daily operations, the business can have problems if they leave. If a large part of revenue comes from one or two big clients, losing one could greatly hurt profits.

Not having clear systems or standard processes increases the risk. This makes it hard for a new owner to keep things running smoothly. To address these challenges, buyers should ask for a clear transition plan. If possible, they should negotiate a seller stay-on period. This will help ensure a smooth handover of relationships and operational knowledge.

Legal and Compliance Issues: Avoiding Hidden Liabilities

Legal and compliance issues are another critical area that can expose buyers to significant risk if overlooked. Pending lawsuits, customer disputes, or employee claims can quickly turn into costly liabilities once ownership changes hands. It’s important to check that all business licenses and permits are up to date and transferable. If they are not, it can disrupt operations or stop business activities completely.

It’s important to follow industry regulations, especially in healthcare, finance, food, and construction. Violating these rules can lead to high fines or harm to your reputation. Additionally, environmental or zoning concerns can lead to unexpected expenses or legal complications down the road. To protect your investment, it is wise to have a qualified attorney review all contracts and legal documents. This should be done before you finalize the purchase.

Operational Inefficiencies and Hidden Costs

Operational inefficiencies and hidden costs can quietly erode profitability and create major challenges for new owners. Some of these issues are not easy to see. However, they can greatly affect the business’s money health and how well it runs. Key areas to watch include:

· Outdated systems, equipment, or technology: May require immediate investment just to remain competitive, leading to unplanned expenses.

· High employee turnover: Could indicate management or cultural problems that disrupt productivity and customer relationships.

· Inflated inventory or excessive supplier costs: Might signal poor purchasing controls or obsolete stock that may need to be written off.

· Hidden obligations: Maintenance costs, unfavorable leases, or undisclosed debt can strain cash flow and reduce the business’s true value.

To find these challenges, buyers should ask for an operational audit. This will help them understand daily operations and possible problems before making a purchase.

Red Flags When Buying a Business Can Be Avoided

Spotting red flags when buying a business doesn’t mean you should walk away from every deal. It’s about making smart and confident choices. The key is to spot potential risks early. This way, you can negotiate from a strong position. You can also invest in a business with long-term potential. Taking a cautious, professional approach with the guidance of experienced advisors such as business brokers, accountants, and attorneys can make all the difference in avoiding costly surprises after closing.

At V-AID Group, we are a top business brokerage in the DFW area. Since 2001, we have focused on selling privately held companies. We work with small to lower middle market businesses. These are also called Main Street and lower mid-size businesses. Their selling prices range from $250,000 to $25 million. We conduct thorough due diligence prior to listing businesses and ensure that all necessary documents are provided, allowing prospective buyers to complete a comprehensive review of financials, operations, and legal compliance.

By giving clear and accurate information, we create a transparent process. This helps people make informed decisions and ensures smooth transactions. If you are thinking about buying a business, contact V-AID Group today. We can help you use our experience and guidance. This will make sure your next purchase is smart, safe, and profitable.

Read More

Financial Readiness for Business Buyers

Buying a business can be one of the most rewarding financial decisions you ever make, but it’s also one of the most demanding. While it’s easy to get excited about potential cash flow, independence, and growth opportunities, the reality is that acquiring a business (especially with financing) involves intense financial scrutiny. Lenders, sellers, and even landlords will want to know you’re not just serious, but financially capable of handling the risk. Before you dive into listings or approach a bank, it’s crucial to take a hard look at your personal financial readiness. In this post, we’ll walk through the key factors that determine whether you’re truly ready to buy a business, especially if you plan to use financing to make it happen.

Understand What ‘Financial Readiness’ Really Means

When it comes to buying a business, being “financially ready” means more than just having some cash in the bank. It means you’re in a strong enough financial position to secure financing, support the business during its transition, and weather potential bumps in the road. Financial readiness is about being loan-worthy in the eyes of a lender and trustworthy to a seller who may be offering financing or staying involved in the transition. It also means being able to take over existing obligations, such as leases or vendor contracts, that may require additional approvals. Ultimately, it’s about reducing risk: both your own and that of any stakeholders involved in the transaction.

Conduct a Financial Readiness Self-Assessment

Before moving forward with a purchase or loan application, take time to do a thorough financial readiness self-assessment. This will help you identify any gaps and avoid surprises later in the process. Start with your credit score, is it 640 or above? If not, improving it should be your first priority. Next, ask yourself whether you have enough liquid assets for a down payment and working capital. Most lenders will expect you to put in at least 15% to 20% of the purchase price, plus have extra cash on hand to support the business post-close.

Evaluate your personal debt as well. If you’re carrying high credit card balances or large personal loans, that could reduce your borrowing capacity or raise red flags. Also consider whether you can cover your personal living expenses for 6–12 months without relying on the business in its early stages. Finally, gather your financial documents, tax returns, bank statements, and a personal financial statement, and review them from a lender’s perspective. Are they organized and accurate? Would they reflect a borrower who’s ready and reliable? If you can confidently check off all these areas, you’re likely in a strong position to begin conversations with lenders or brokers.

If You’re Not Ready Yet, Don’t Worry

If your self-assessment reveals some weak spots, don’t worry, there are clear steps you can take to improve your readiness. Start by focusing on your credit health: pay down high-interest debts, make all payments on time, and consider working with a credit repair specialist if necessary. At the same time, work to increase your savings. This could mean cutting personal expenses or selling underutilized assets. Reducing your personal debt not only improves your financial profile but also lowers your monthly obligations, making it easier to qualify for financing.

If liquidity is a major issue, consider bringing in a partner or investor who can contribute capital in exchange for equity or a return on investment. You might also explore creative financing options such as a Home Equity Line of Credit (HELOC) or look for smaller, more affordable businesses that require less upfront capital. In some cases, it may make sense to delay your purchase by six to twelve months while you strengthen your position. Remember, buying a business is a major commitment. Taking the time now to prepare properly will significantly increase your chances of success, not just in securing financing, but in running a profitable and sustainable business.

Know How Much Money You’ll Need

One of the most common mistakes aspiring business buyers make is underestimating how much capital they’ll actually need, not just to buy the business, but to keep it running and growing. The most obvious cost is the down payment, which is typically 15-20% of the purchase price for an SBA loan. This money usually needs to come from your own savings or liquid assets, although there are some creative strategies (like retirement rollovers or investor partnerships) that can help bridge the gap.

Beyond the down payment, you’ll also need working capital reserves. These funds are crucial for covering payroll, inventory, rent, and other expenses in the first few months of ownership, especially if the business has seasonal swings or cash flow lags. A good rule of thumb is to have at least three to six months of operating expenses set aside. Don’t forget about transactional and professional fees either. Legal reviews, due diligence, loan origination fees, and closing costs can add up quickly, sometimes totaling tens of thousands of dollars, depending on the deal size. Planning ahead for all these costs helps ensure you’re not scrambling for funds during the most critical phase of your ownership journey.

Documentation You’ll Be Expected to Provide

Once you begin the process of financing a business purchase, be prepared to supply a significant amount of personal and financial documentation. Lenders want a clear picture of your financial standing before they approve any funding, and sellers (especially if offering seller financing) may also request some of the same information. At a minimum, you’ll need to provide a Personal Financial Statement (PFS), which outlines your assets, liabilities, income, and expenses. In addition, most lenders require three years of personal tax returns to assess income stability and financial behavior over time.

You should also be ready to share recent bank statements to verify your available funds for a down payment and working capital. If you plan to use funds from a retirement account, home equity, or a partner, documentation of those sources will be needed as well. Buyers often overlook the role of the landlord in this process, but it’s critical if the business operates out of a leased location. In many cases, the lease must be transferred or re-negotiated as part of the transaction, and landlords may conduct their own due diligence. That means they’ll likely review your net worth, liquidity, and credit history before approving the lease assignment. If your finances raise concerns, the landlord may request a larger security deposit, a personal guaranty, or even reject the lease transfer altogether, so be prepared for that additional layer of scrutiny.

Understand Lender Expectations

Lenders don’t just look at numbers, they look at the whole picture. Beyond credit scores and bank statements, they want to see that you’re a capable, low-risk borrower who can successfully operate the business you’re buying. One key element is your professional background. If you have direct industry experience, that’s a major plus. But even if you don’t, transferable skills such as leadership, operations, or financial management can make a big difference in the eyes of a lender. Being able to articulate how your skills align with the business you’re acquiring can strengthen your loan application considerably.

Lenders also want to see that you’re personally invested in the success of the business. This often translates into having “skin in the game”, your own money committed to the deal. A strong down payment shows that you’re serious and helps mitigate the lender’s risk. In addition, lenders look for clean, well-documented business financials from the seller. If the business’s books are a mess or show inconsistent revenue, that could kill the deal, regardless of your own financial strength. Finally, lenders will evaluate the cash flow of the business to determine whether it can comfortably service the loan payments while still providing you with a livable income. All of these factors come together to shape a lender’s decision, and understanding their expectations in advance will give you a major advantage as you prepare to buy.

Final Thoughts on Financial Readiness

Buying a business goes far beyond enthusiasm and ambition. Buying requires a clear, well-documented picture of your financial health and readiness. From assessing your credit and liquidity to understanding lender expectations and hidden costs, every step plays a crucial role in setting the stage for a successful acquisition. Whether you’re ready now or need more time to strengthen your position, approaching the process with diligence and foresight will not only improve your chances of securing financing but also help ensure that your future business venture is built on a solid financial foundation.

Read More

Small Business Private Lenders: Tips for Finding the Right Lender

Small business private lenders can make or break a business transaction. Buying a business is a complex journeys that involve the identification of just the right opportunity, negotiation of terms, and finalization of the purchase. This, of course, constitutes a very important part of such a process: finding financing, given that this determines not only the feasibility of the acquisition but also the financial health of the new venture.

The right financing opens the door to growth and success, while the wrong choice can lead to a myriad of challenges later on. In this blog, we try walking the prospective business buyer through critical determinants for the right lender-one who can guarantee favorable rates, responsive communication, and expert support that assure a smooth, successful acquisition.

The Importance of Choosing The Right Lenders

The lenders are very important in the process of acquisition, as they represent the main source of finance for buyers. Lenders evaluate the financial viability of the acquisition by determining the creditworthiness of the buyer, the financial health of the business, and the conditions of the market in general. Detailed documentation and analysis are generally required to establish that the buyer is in a position to sustain the loan and that the business has the potential for profitability.

In addition to providing the required funds, lenders also guide transactions by counseling buyers through the complexity of financing options and structuring deals according to their needs and requirements. This would, therefore, make much difference when there is a strong partnership with a proper lender for the acquisition process in order to have a successful transition.

Different Lenders, Different Rates

Securing the best interest rate is one of the major aspects of purchasing a business in order to minimize overall financing costs. A small difference in rates makes all the difference in both your monthly payments and the total amount paid over the course of the loan. Many times, interest rates can be all over the board depending on the lender due to their own practices in assessing risk associated with loans, market conditions, and specific terms of the loan itself.

Comparisons should be made by buyers by getting quotes from a number of different lenders, carefully considering the APR interest rate plus any fees. Also, consider prepayment penalties and any flexibility in the terms with regard to repayment options, so that you make a fully-rounded decision that will meet your financial needs.

Communication is Key

Communication at the proper time holds the key to any business acquisition process; it keeps the parties informed at each and every stage of the transaction. A responsive lender can go a long way in making such a transaction far smoother, addressing any questions, or providing documentation and necessary support to work out complex financing options. Such a level of engagement builds confidence and can even speed up the process of approvals, which is very important in today’s competitive market.

Viewed negatively, the absence of a response may lead to several delays that may compromise a sale or lead to misunderstandings over loan terms or maybe even a lost opportunity. For instance, if a lender is not in a position to promptly respond to requests for information, the pace of negotiation might be slowed down, or buyers might remain without some crucially important knowledge, which is very important in making valid decisions regarding this type of acquisition.

Flexibility Makes All the Difference

Flexibility is one of the important attributes a lender should have, considering that every business acquisition carries with it different circumstances and challenges that need particular financing solutions. A lender who is willing and able to adapt to the specific needs of the buyer-be it accommodating a fluctuating cash flow, adjusting repayment terms, or offering alternative financing structures-can indeed make quite a difference in the success of the acquisition process as a whole.

Creative financing options can include seller financing, or tailored repayment plans, which could better equip buyers to overcome surprises that stand in the way of maximizing their investment. A flexible lender can help the buyer tap into options that would better fit their personal financial circumstances and make the business more sustainable and profitable.

Transparency Sets Clear Expectations

Transparency about lending is paramount to ascertain that buyers are aware of the terms and conditions of financing.

This covers things like interest rates, payment schedules, fees, and even penalty clauses in clearly understandable language so that no surprises occur along the way. It is the right of the consumer to ask questions before signing up for any form of loan, including but not limited to how much it costs as a whole, the implications of variable rates as opposed to fixed rates, and lastly, any other hidden charges that might come up in due course.

Best Questions to Ask Your Small Business Private Lenders

You should be proactive, but not rush to find the right lender for your business acquisition. First, get recommendations from a trusted advisor, including a business broker or financial consultant. Second, research online to identify an appropriate lender that specializes in business financing.

Jot down a shortlist, follow through, and schedule an initial consultation to see if they will be a good fit for you. In these meetings, ask the following pertinent questions:

- What types of loans do you offer for business acquisitions?

- Can you provide a detailed breakdown of fees and interest rates?

- How long does the approval process typically take?

- What is your experience with financing similar transactions?

- How do you approach customer service and communication during the loan process?

- Are there any prepayment penalties or flexibility in repayment options?

- Can you outline the documentation required for the loan application?

- What criteria do you use to assess creditworthiness for business loans?

Begin Your Small Business Lending Adventure with V-AID

In conclusion, selecting the right lender is among the most crucial decisions in the acquisition phase of a business that may affect one’s future financially, as well as the overall success of the new venture. By placing interests such as interest rates, responsiveness, transparency, and flexibility first, buyers are put in a better position to make informed choices that best match their particular needs.

V-AID specializes in guiding qualified buyers through the financing process. We leverage our extensive network of lenders to connect you with the most suitable options, ensuring you secure competitive rates and exceptional service.

Our team is dedicated to helping you navigate this crucial aspect of your business acquisition, so you can focus on achieving your goals. Let us be your buying guide and assist you in selecting the ideal lender to set you on the path to success.

Read More