Asset Sale vs. Stock Sale: Key Differences Every Business Owner Should Know

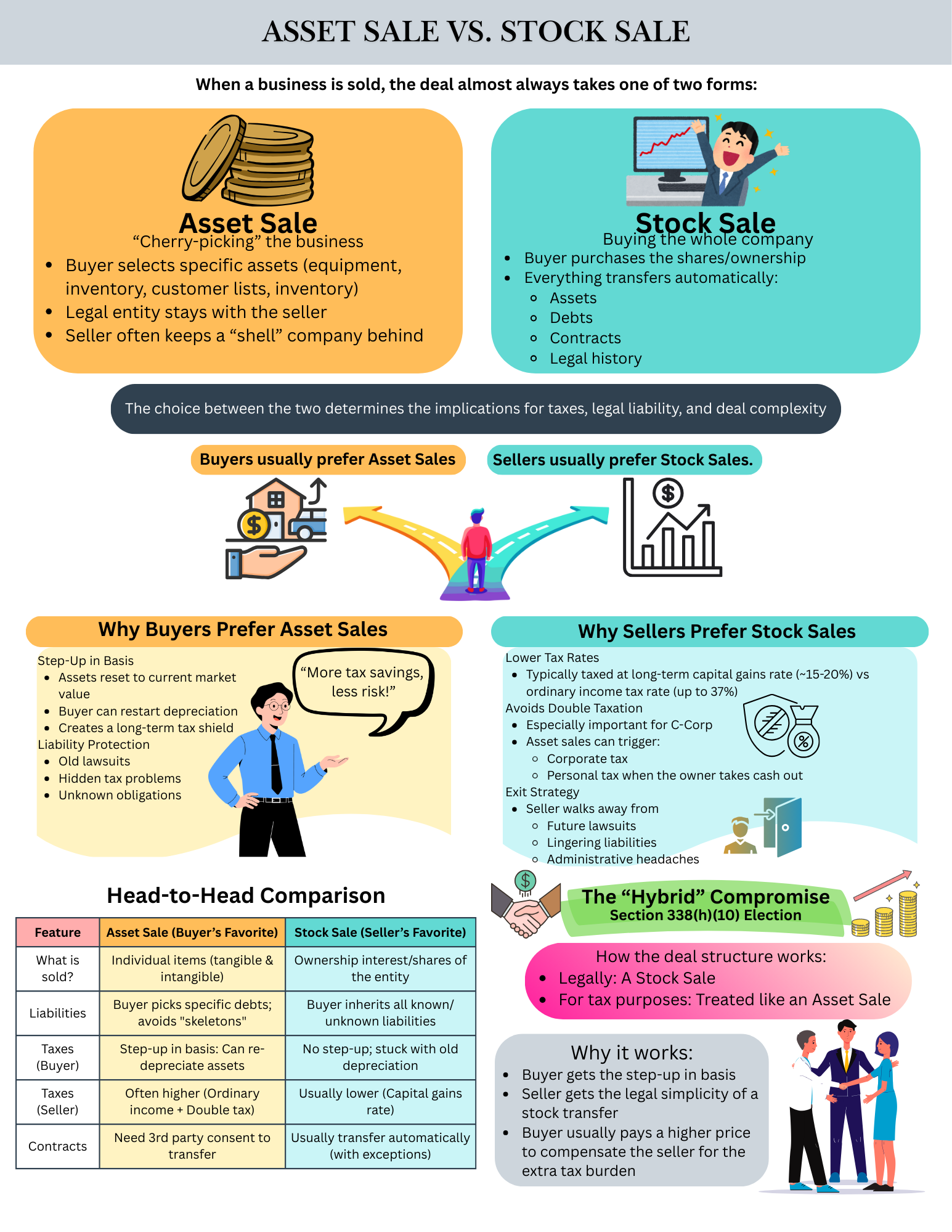

When a business is sold, the transaction is almost always structured as either an asset sale or a stock sale. While the distinction may sound technical, the structure of the deal has major implications for taxes, legal risk, and how smoothly ownership transfers. In most transactions, buyers lean toward asset sales, while sellers typically prefer stock sales.

In an asset sale, the buyer purchases selected pieces of the business, such as equipment, inventory, customer lists, or intellectual property, rather than the company itself. The legal entity remains with the seller, often holding any leftover liabilities. In a stock sale, the buyer purchases the ownership interests of the company, meaning everything inside the entity transfers automatically, including assets, contracts, debts, and legal history.

Buyers generally favor asset sales because they offer greater protection and tax advantages. Purchasing assets allows buyers to “step up” the value of those assets for tax purposes, enabling new depreciation schedules that can reduce taxable income over time. Asset sales also allow buyers to leave behind unwanted liabilities, minimizing exposure to unknown risks.

Sellers, on the other hand, usually prefer stock sales because they are simpler and often more tax-efficient. Stock sales are typically taxed at long-term capital gains rates and can help sellers avoid double taxation, especially in C-corporation deals. Just as importantly, a stock sale allows the seller to make a clean exit, walking away from the entity and its future obligations.

In some cases, buyers and sellers compromise using a Section 338(h)(10) election, which treats the transaction as a stock sale legally but an asset sale for tax purposes. This structure gives buyers the tax benefits they want while preserving the simplicity of a stock transfer, often with a higher purchase price to balance the tax impact for the seller.