What Is Seller’s Discretionary Earnings (SDE), and Why Should Business Owners Care?

When business owners begin thinking about selling, one of the first questions they ask is, “What is my business worth?”

Many owners would usually assume that the answer is based on the annual revenue, the amount they’ve invested over the years, or what similar businesses are listed for online. However, in reality, most small businesses are valued very differently.

For the majority of “Main Street Businesses” that are typically purchased by individual buyers or financed through SBA loans, the most important number is Seller’s Discretionary Earnings (SDE). Understanding how SDE works can help business owners set realistic expectations, avoid pricing mistakes, and ultimately sell their business faster and for the highest market-supported value.

What Is Seller’s Discretionary Earnings (SDE)?

Seller’s Discretionary Earnings (SDE) measures the total economic benefit an owner-operator receives from a business Rather than focusing solely on accounting profit, SDE adjusts the company’s financials by adding back certain discretionary, non-recurring, or owner-specific expenses to provide a clearer picture of the cash flow available to a new owner.

It begins with the business’s pre-tax net income and adds back certain expenses that may not continue under new ownership.

Common add-backs include:

- Owner’s salary, payroll taxes, and benefits

- Personal expenses paid through the business

- One-time or unusual expenses

- Interest expense

- Depreciation and amortization

- Non-recurring legal or professional fees

- Other discretionary expenses that would not reasonably transfer to a new owner

The goal of SDE is to show the true earning power of the business for someone who purchases and operates it. Because most Main Street businesses rely heavily on the owner’s day-to-day involvement, SDE is generally the preferred earnings metric used for valuation. Larger lower middle-market businesses, on the other hand, are more commonly evaluated using EBITDA because they tend to have more established management teams and are less dependent on a single owner.

How Is SDE Calculated?

While every business is unique, a simplified calculation looks like this:

Pre-Tax Net Income

+ Owner Compensation

+ Interest

+ Depreciation

+ Amortization

+ Qualified Discretionary or Non-Recurring Expenses

= Seller’s Discretionary Earnings (SDE)

The purpose of these add-backs is to normalize the business’s earnings by removing expenses that may not continue under new ownership. This allows buyers to evaluate the true earning potential of the business rather than the financial decisions of the current owner. However, not every expense qualifies as an add-back.

To be considered, the expense should generally be discretionary, non-recurring, or unique to the current owner. Routine operating expenses (such as payroll for employees, rent, utilities, inventory, insurance, and marketing) typically remain necessary to operate the business and therefore are not added back. Each adjustment should be supported by historical financial records and a reasonable explanation. Buyers, lenders, and appraisers expect these adjustments to be documented rather than based on estimates or verbal statements.

Why Main Street Businesses Are Usually Valued Using SDE

There is no single method for valuing every business. Different industries, company sizes, and transaction types require different valuation approaches.

For most Main Street businesses, buyers are purchasing an owner-operated business that generates income. Because the owner’s involvement often plays a significant role in the business’s success, buyers focus primarily on the cash flow they can reasonably expect to earn after taking over operations.

For that reason, business brokers commonly rely on two primary valuation tools:

- Seller’s Discretionary Earnings (SDE) to determine the business’s normalized cash flow.

- Direct Market Data Method (DMDM) to compare the business against similar businesses that have actually sold.

Similar to a residential real estate appraisal, the Direct Market Data Method analyzes completed sales of comparable businesses, not asking prices, to determine the multiples buyers have actually paid. Factors such as industry, size, profitability, location, growth potential, and risk are all considered when identifying comparable transactions.

When SDE and the Direct Market Data Method are used together, they generally provide the most probable selling price that today’s market is willing to support.

Why Revenue Alone Doesn’t Determine Value

One of the most common misconceptions is that a business is worth a multiple of its annual revenue. While revenue measures how much money a business brings in through sales, it does not show how much the owner actually earns after paying operating expenses. A business with high revenue but low profitability may be worth less than a business with lower revenue and stronger cash flow.

For example:

- Business A generates $2 million in annual revenue but produces only $150,000 in SDE.

- Business B generates $1 million in annual revenue but produces $300,000 in SDE.

Although Business A generates twice the revenue, many buyers would place a higher value on Business B because it produces significantly stronger cash flow.

This illustrates why buyers focus primarily on a business’s earning potential rather than its sales volume. In many cases, a business with lower revenue but higher Seller’s Discretionary Earnings is worth more than a business with substantially higher revenue and lower profitability.

Why the Income Approach is Less Practical for Main Street Businesses

Business owners often hear about valuation methods such as the Income Approach or Discounted Cash Flow (DCF) analysis. While these methods are widely accepted in business valuation, they are generally more appropriate for larger companies with stable financial reporting, professional management teams, and predictable long-term cash flows.

Most Main Street businesses do not fit those characteristics as many are heavily dependent on the owner’s day-to-day involvement, have fluctuating earnings, and experience changes in expenses from year to year. As a result, forecasting future cash flow can be highly subjective, making an income-based valuation less practical for many small businesses.

Instead, buyers, lenders, and business brokers typically place greater emphasis on historical financial performance and actual market transactions. This is why Seller’s Discretionary Earnings (SDE), combined with the Direct Market Data Method (DMDM), is often the preferred approach for valuing owner-operated Main Street businesses, as it reflects both documented earnings and what buyers have actually paid for comparable businesses.

Does Real Estate Affect the Business Valuation?

To answer this question, it depends on if the real estate is leased because the business is typically valued separately from the property. Buyers evaluate the business based on its cash flow while also considering the lease terms, rental rate, remaining lease term, and any renewal options.

If the seller owns the commercial property, there are generally two separate assets involved:

- The operating business

- The commercial real estate

Because these assets generate value in different ways and are often financed separately, each is typically valued independently. Depending on the seller’s goals and the buyer’s financing, the business may be sold with or without the real estate.

When calculating Seller’s Discretionary Earnings (SDE), the business’s rent expense should also reflect fair market value. If the owner is paying themselves above-market or below-market rent, business brokers will often normalize the rent to current market rates. This adjustment helps present a more accurate picture of the business’s earning potential and allows buyers to evaluate the business based on what they can reasonably expect to pay after the sale.

Why Accurate Financial Records Matter

One of the biggest challenges in business valuation occurs when owners estimate their earnings based on memory rather than documented financial records.

Statements like:

- “I usually spend about…”

- “That expense averages around…”

- “I don’t think we spent that much every year.”

are difficult for buyers, lenders, and brokers to rely on because they cannot be independently verified.

An accurate Seller’s Discretionary Earnings (SDE) calculation should be supported by historical financial statements, tax returns, profit and loss statements, payroll records, bank statements, and other supporting documentation. If an expense truly qualifies as an add-back, it should be clearly identified and supported with evidence whenever possible.

Furthermore, business valuations are based on documented financial performance, not verbal estimates or assumptions. Well-organized financial records can increase buyer confidence, simplify due diligence, reduce the likelihood of valuation disputes, and help support a market value that buyers and lenders can justify.

Understanding the Difference Between Perceived Value and Market Value

It is very common for business owners to often develop an emotional connection to the businesses they have spent years building; the time, effort, and sacrifices invested are real, but the market ultimately determines the most probable value based on documented earnings, buyer demand, and perceived risk. In other words, a business is not worth what the owner hopes it is worth, worth what it costs to build, nor is it worth what similar businesses are listed for online. Ultimately, a business is worth what a qualified buyer is willing to pay based on verified financial performance, comparable market transactions, and the level of risk associated with the opportunity.

Understanding Seller’s Discretionary Earnings (SDE) is one of the most important steps in setting realistic expectations and preparing for a successful sale. Owners who understand how buyers evaluate businesses are better positioned to price appropriately, attract qualified buyers, and maximize value during negotiations. Before taking a business into the market, having your financials properly recast and your Seller’s Discretionary Earnings accurately calculated is one of the best investments you can make. Well-prepared financials build buyer confidence, streamline due diligence, and help support a valuation that reflects what the market is truly willing to pay.

Read More

Why Some Businesses Sell Quickly While Others Sit on the Market

What Makes a Business Easy to Buy and Easy to Sell?

If you’re thinking selling a business in today’s market, one of the most important questions to ask is whether the company is easy for a buyer to acquire. While strong revenue and profitability certainly matter and often help explain why some businesses sell quickly, today’s buyers are looking beyond earnings alone. They want businesses with clean financials, transferable operations, organized records, and financing options that support a smooth transaction.

Today’s business buyers are conducting more due diligence than ever before. Lenders are carefully reviewing financial performance before approving SBA financing, and buyers are scrutinizing every aspect of a business acquisition before making an offer.

As a result, some businesses attract immediate interest and receive multiple offers, while others struggle to gain traction despite producing healthy profits.

The difference, and often the reason why some businesses sell quickly while others sit on the market, often comes down to one simple question:

How easy is the business to buy and, ultimately, how easy is it to sell?

The businesses that attract the strongest buyer interest are often those that reduce uncertainty and make it easy for a buyer to envision a successful transition.

Clean Financials Make a Business Easier to Sell

One of the first things buyers evaluate when considering a business for sale is the financial performance of the company.

Today’s buyers expect detailed and accurate financial reporting. Most will review several years of tax returns, profit and loss statements, balance sheets, payroll reports, and bank statements before moving forward.

When financial records are incomplete, inconsistent, or difficult to understand, buyers become cautious. Questions arise regarding profitability, cash flow, and the overall reliability of the information being presented.

Businesses with clean financials immediately stand out. Clear reporting helps buyers verify earnings and simplifies the due diligence process.

In many cases, organized financial statements not only increase buyer confidence but can also positively influence business valuation because they reduce perceived risk.

Simply put, buyers are more likely to pursue a business acquisition when they trust the numbers.

Why Organized Business Records Matter to Buyers

Financial statements are only one piece of the puzzle.

Buyers increasingly expect organized records throughout the business, including:

-Equipment inventories

-Lease agreements

-Vendor contracts

-Employee documentation

-Customer agreements

-Licenses and permits

-Operating procedures

When records are organized and readily available, buyers can quickly verify information and move through due diligence more efficiently.

On the other hand, transactions often slow down when sellers spend weeks locating documents or attempting to recreate missing information.

Organized records demonstrate professionalism and help create confidence that the business has been managed responsibly.

For owners preparing to sell a business, maintaining accurate records can significantly improve the buyer experience.

Buyers Want Businesses That Can Run Without the Owner

One of the most important questions buyers ask is:

“What happens when the owner leaves?”

Businesses that depend heavily on the owner’s personal involvement often face greater scrutiny during the sale process.

The most attractive businesses have systems and procedures that can be transferred to a new owner.

Examples include:

-Written operating procedures

-Established employee responsibilities

-Consistent customer acquisition methods

-Defined management structures

-Repeatable workflows

When buyers see that a business can continue operating successfully after the owner exits, they feel more comfortable moving forward.

Transferable operations reduce risk and increase the pool of qualified buyers.

In today’s market, businesses that can function independently of the owner are often easier to sell, which is one of the key reasons why some businesses sell quickly while others struggle to attract buyers.

Why Low Owner Dependence Increases Business Value

Many successful businesses are built through years of personal effort and involvement. However, buyers often view excessive owner dependence as a risk.

Common signs of owner dependence include:

-The owner manages all key customer relationships.

-The owner handles every sales function.

-Major decisions require the owner’s approval.

-Critical business knowledge exists only in the owner’s head.

When buyers encounter these situations, they naturally wonder whether revenue and operations will remain stable after the transition.

Businesses with empowered employees, documented processes, and delegated responsibilities typically generate greater confidence among buyers.

Reducing owner dependence is one of the most effective ways to improve both business valuation and marketability.

Why SBA Financing Makes a Business More Attractive

Financing plays a major role in business acquisitions.

Many transactions today involve SBA financing because it allows qualified buyers to purchase a business with less upfront capital.

As a result, businesses that are considered “bankable” often attract a larger pool of buyers.

A business that qualifies for SBA financing typically has:

-Consistent cash flow

-Verifiable earnings

-Stable operating history

-Reasonable debt levels

-Clean financial reporting

When buyers know a business is likely to qualify for an SBA loan, they are often more willing to pursue the opportunity.

Conversely, businesses that cannot obtain financing may require substantially larger cash investments, limiting the number of qualified buyers.

Making a business financeable can dramatically improve buyer interest and increase the likelihood of a successful transaction.

Seller Financing Can Help Close More Deals

Although not every transaction includes seller financing, buyers generally view some level of seller participation positively.

A seller note can demonstrate confidence in the business while helping bridge financing gaps that occasionally arise during negotiations.

In many successful transactions, the seller is willing to carry a modest note for a qualified buyer to help complete the deal.

This flexibility can benefit both parties by making the transaction easier to finance and helping buyers feel more comfortable moving forward.

Seller financing is rarely the primary driver of a sale, but it can often help good deals reach the finish line.

Well-Maintained Assets Create Strong First Impressions

The condition of business assets can significantly influence buyer perception.

Buyers carefully evaluate:

-Equipment

-Furniture and fixtures

-Vehicles

-Technology systems

-Production assets

-Specialized tools

Businesses with assets in good condition generally create a stronger first impression.

Well-maintained equipment signals responsible ownership and reduces concerns about unexpected repair or replacement costs after closing.

While buyers understand that no asset remains brand new forever, they appreciate businesses that have consistently invested in maintenance and upkeep.

A business with clean, functional assets is often easier to market and easier to sell.

Modest Transition Support Reduces Buyer Risk

Many buyers, particularly first-time business owners, are concerned about the transition period following a sale.

This is why modest post-transaction support can make a business significantly more attractive.

Buyers appreciate sellers who are willing to provide reasonable training and consultation after closing.

This support may include:

-Employee introductions

-Customer introductions

-Vendor transitions

-Operational training

-General consultation during the transition period

Most buyers are not seeking long-term involvement from the seller. They simply want reassurance that guidance will be available during the initial ownership transition.

A willingness to provide post-sale support often increases buyer confidence and helps transactions close more smoothly.

Realistic Seller Expectations Help Businesses Sell Faster

One of the most overlooked factors in selling a business is the seller’s mindset.

Buyers appreciate working with sellers who understand market conditions and approach negotiations realistically.

Being realistic does not mean accepting an unreasonable offer. It means recognizing that business acquisitions involve financing requirements, due diligence, negotiation, and compromise.

Sellers who remain flexible and responsive often achieve better outcomes than those who focus exclusively on a specific purchase price.

The strongest transactions occur when both parties are committed to finding a structure that works for everyone involved.

Final Thoughts: Making a Business Easier to Sell

A business does not need to be perfect to attract serious buyers.

However, businesses that are easy to understand, finance, and transition consistently generate stronger buyer interest.

If a business owner is considering a sale in the next few years, focusing on the factors buyers care about most can significantly improve marketability:

-Clean financials

-Organized records

-Transferable operations

-Low owner dependence

-SBA financing eligibility

-Flexible deal structures

-Well-maintained assets

-Reasonable transition support

-Realistic seller expectations

The businesses that receive the strongest offers are not always the fastest growing. More often, they are the businesses that reduce uncertainty, inspire confidence, and make it easier for buyers to envision a successful transition.

By preparing well before going to market, owners can increase buyer interest, improve valuation, and position themselves for a smoother and more successful sale.

Frequently Asked Questions as to Why Some Businesses Sell Quickly

What makes a business easier to sell?

Businesses with clean financials, organized records, strong cash flow, transferable operations, and low owner dependence are generally easier to sell because buyers can more easily evaluate and finance the opportunity.

Does SBA financing help sell a business?

Yes. Businesses that qualify for SBA financing often attract a larger pool of buyers because purchasers can finance a portion of the acquisition rather than paying entirely in cash.

Why do buyers care about owner dependence?

Buyers want confidence that the business will continue performing after the seller exits. Excessive owner dependence increases risk and can negatively impact buyer interest and valuation.

Does a seller need to offer financing?

No. However, a seller willing to carry a modest note for a qualified buyer can often help facilitate a transaction and increase buyer confidence.

How important are financial records when selling a business?

Financial records are one of the most important aspects of any transaction. Clean, organized financial statements help buyers verify earnings and complete due diligence more efficiently.

What role does post-sale training play in a business sale?

Post-sale training and consultation help ensure a smooth transition, reduce buyer risk, and can make a business more attractive to prospective purchasers.

Read More

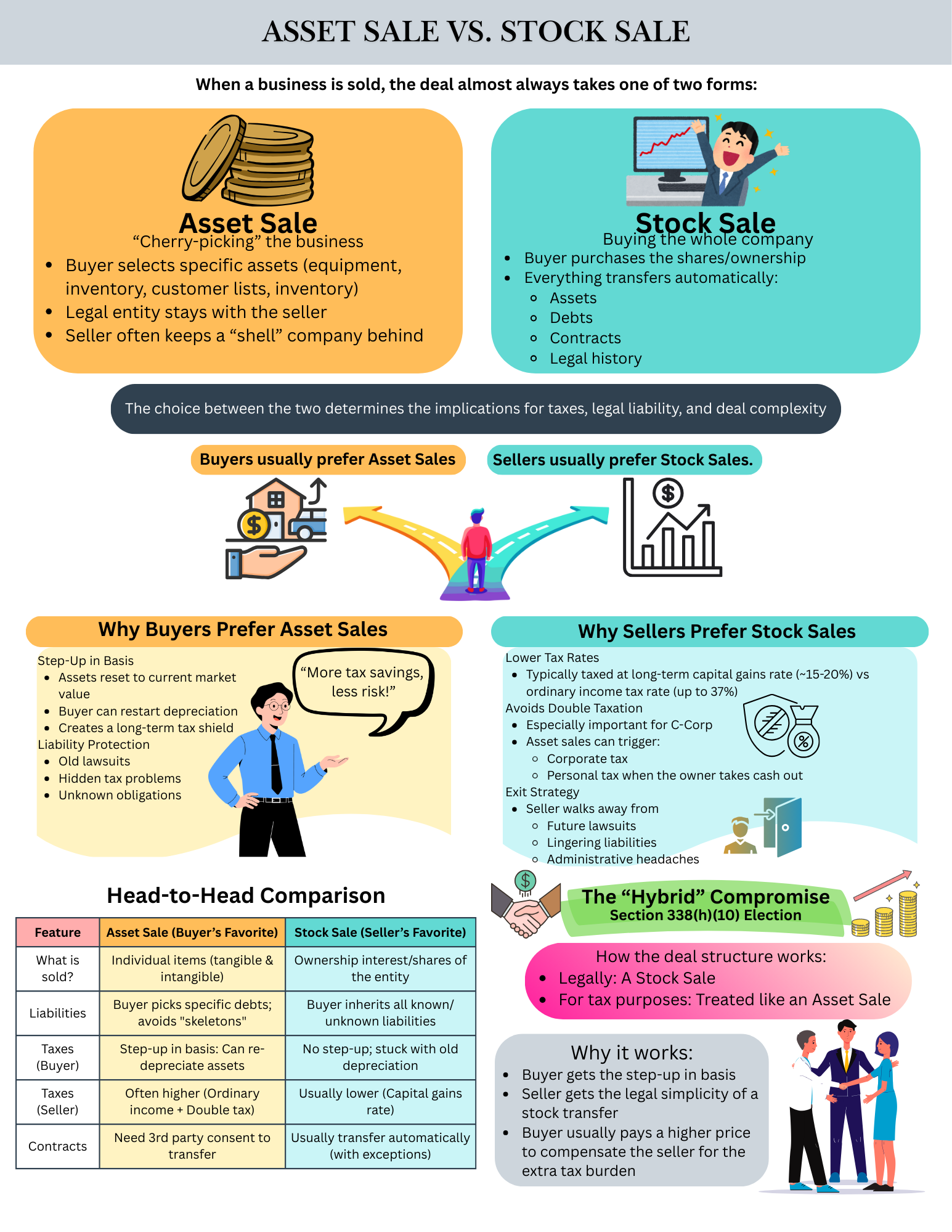

Asset Sale vs. Stock Sale: Key Differences Every Business Owner Should Know

When a business is sold, the transaction is almost always structured as either an asset sale or a stock sale. While the distinction may sound technical, the structure of the deal has major implications for taxes, legal risk, and how smoothly ownership transfers. In most transactions, buyers lean toward asset sales, while sellers typically prefer stock sales.

In an asset sale, the buyer purchases selected pieces of the business, such as equipment, inventory, customer lists, or intellectual property, rather than the company itself. The legal entity remains with the seller, often holding any leftover liabilities. In a stock sale, the buyer purchases the ownership interests of the company, meaning everything inside the entity transfers automatically, including assets, contracts, debts, and legal history.

Buyers generally favor asset sales because they offer greater protection and tax advantages. Purchasing assets allows buyers to “step up” the value of those assets for tax purposes, enabling new depreciation schedules that can reduce taxable income over time. Asset sales also allow buyers to leave behind unwanted liabilities, minimizing exposure to unknown risks.

Sellers, on the other hand, usually prefer stock sales because they are simpler and often more tax-efficient. Stock sales are typically taxed at long-term capital gains rates and can help sellers avoid double taxation, especially in C-corporation deals. Just as importantly, a stock sale allows the seller to make a clean exit, walking away from the entity and its future obligations.

In some cases, buyers and sellers compromise using a Section 338(h)(10) election, which treats the transaction as a stock sale legally but an asset sale for tax purposes. This structure gives buyers the tax benefits they want while preserving the simplicity of a stock transfer, often with a higher purchase price to balance the tax impact for the seller.

Selling Your Business? 7 Common Value Slashers

The Silent Threat to Business Owners

Most business owners think their company’s value is based mainly on revenue, profit, or how busy the business looks from the outside. But what really hurts value usually isn’t obvious on a financial statement. It hides in the way the business is run, how dependent it is on the owner, how organized (or disorganized) operations are, and how much risk sits quietly inside the company. Those issues often don’t cause daily problems, so they’re easy to ignore, until a buyer, bank, or investor starts digging.

That’s when many owners discover the truth: value isn’t usually lost in one big moment. It slowly slips away because of problems that felt “under control” for years.

In this article, we’ll break down seven common hidden value slashers most businesses have, why they matter, and what you can do to fix them before they cost you real money.

The 7 Value Slashers When Selling Your Business

#1 Owner Dependency: When the Business Can’t Breathe Without You

One of the biggest hidden threats to valuation is when the business is overly dependent on the owner. If the company can’t function when you take a vacation… if every customer insists on speaking only with you… if every decision has to cross your desk… congratulations, you haven’t just built a business, you’ve built a job you own.

Buyers don’t want to purchase someone else’s workload. They want to acquire an operation that runs predictably, consistently, and profitably without being tethered to one individual. When success is tied directly to your presence, expertise, or relationships, a buyer sees risk… and risk always reduces price, leverage, and deal structure.

The warning signs often feel like compliments:

“You’re the only one who really understands the business.”

“Nothing moves forward unless you approve it.”

“Our customers trust you more than anyone else.”

Those statements sound flattering, but they’re actually indicators that the business does not stand on its own. In due diligence, that doesn’t translate to admiration, it translates to uncertainty, transition concerns, and fear of revenue loss once you exit.

The Fix: Start building a business that can operate without you. That means developing real leadership depth, delegating decision-making authority (not just tasks) and investing in training and documented processes.

Encourage client relationships with your team, not just with you. Create a culture where you are no longer the single point of failure.

The goal is simple: if you step back, the business shouldn’t slow to a crawl… it should continue to perform. When an owner becomes optional rather than essential, valuation increases, confidence rises, and your business becomes the readily transferable, high-value asset it was meant to be.

#2 Limited Operating History: When Success Is Too New to Trust

A business can look and feel exciting when it’s growing fast, but if it hasn’t been around long enough to prove consistency, buyers get cautious. Newly established businesses, or companies with only a short window of strong performance for less than three years, often struggle to justify premium valuations simply because there isn’t enough historical data to prove the results are sustainable.

Buyers aren’t just purchasing today’s success, they’re trying to predict tomorrow’s reliability. Without a track record, that prediction becomes guesswork, and guesswork lowers price.

You’ll also recognize this situation if: your business has only been profitable for a short period, is still stabilizing revenue, recently pivoted its model, or simply hasn’t existed long enough to show multi-year proof of performance. Maybe the growth is real and momentum is strong, but there aren’t enough years of financial statements to demonstrate that it’s durable. From an owner’s perspective, it may feel obvious that success will continue. From a buyer’s perspective, it feels untested.

The Fix: Focus on building credibility and clarity. Maintain clean, accurate, professionally prepared financials from day one. Show consistent month-over-month and year-over-year improvement. Build recurring revenue where possible. Strengthen customer retention and operational stability.

Document why your success is sustainable and not accidental or short-lived. The more predictable and proven your performance becomes, the easier it is for buyers to feel confident… and the higher your valuation climbs.

#3 Messy or Unreliable Financials: When “Good Enough” Becomes Very Expensive

Nothing kills confidence faster in a deal than financials that are unclear, inconsistent, or undocumented. You may know your business is healthy, profitable, and stable, but buyers don’t purchase based on trust; they purchase based on proof.

When your books are disorganized, loads of personal expenses are mixed in, add-backs are questionable, or financial statements don’t align, what feels like “normal” to you looks like risk to a buyer. And in valuation, risk is punished every single time. Deals slow down, legal and accounting costs go up, and more often than not, the purchase price drops or the buyer walks away entirely.

If any of this sounds familiar, you’re not alone: the CPA scrambles at tax time because things haven’t been reconciled, cash flow is “managed from the bank account,” financial reports are months behind, or there’s no consistent narrative explaining performance year over year. Owners sometimes think these issues are “just paperwork.” They’re not.

They are the backbone of credibility. Buyers want to see clear earnings, quality cash flow, and financial discipline. When the numbers don’t tell a clean and verifiable story, buyers assume the worst, even if the business is actually performing well.

The Fix: Clean, professional financials are one of the fastest ways to retain business value. Invest in strong bookkeeping and accounting support. Produce timely monthly financial statements. Separate personal and business expenses. Understand what truly qualifies as an add-back. Build 2–3 years of reliable, well-documented financial history.

In short, make your financials defensible. When buyers see clarity, discipline, and transparency, confidence rises… and so does the price they’re willing to pay.

#4 Customer Concentration: When Too Much Revenue Rests on Too Few Relationships

Customer concentration is one of those value slashers that doesn’t feel like a problem until it becomes one. On the surface, having a small number of high-paying clients can feel like efficiency, stability, and partnership. But from a buyer’s perspective, it’s a flashing red warning light.

When 20%, 30%, or even 50%+ of your revenue comes from one or two key accounts, the buyer isn’t just purchasing your business… they’re essentially gambling on whether those clients will stay after you leave. If they don’t, the business they just bought could collapse overnight. That level of dependency turns what could have been a strong valuation into a discounted, heavily structured, or risky deal very quickly.

The tough reality: if one client has the power to significantly affect your financial health by leaving, renegotiating, or reducing spending, then your business doesn’t truly control its revenue, your client does. Buyers know this. Lenders know this. And in due diligence, they scrutinize it hard.

Even if that anchor client has been loyal for years, even if the relationship feels “rock solid,” buyers think in terms of risk probability, not optimism. High concentration equals uncertainty. Uncertainty equals lower prices, more earn-outs, and tougher negotiations.

The Fix: Diversification is key. Start intentionally widening your customer base so no single client holds your business hostage. Develop a strategy to attract mid-tier accounts rather than depending solely on whales. Where possible, strengthen contracts, extend terms, or create recurring revenue arrangements that lock in stability.

Going to our first value slasher, cultivate deeper client relationships across your organization so loyalty isn’t tied to you personally. Over time, aim for no single customer representing more than 10–20% of total revenue. When your revenue is spread across many reliable customers, your business instantly becomes more resilient, more transferable, and far more valuable in the eyes of a buyer.

#5 Weak or Inconsistent Profit Margins: When Busy Doesn’t Equal Valuable

A surprising number of businesses look strong on the surface; steady revenue full workloads, phones ringing, yet when you peel back the layers, the margins tell a very different story. Buyers don’t pay for how busy the business is; they pay for how profitably the business operates.

Thin or inconsistent margins signal fragility. They suggest pricing pressure, operational inefficiency, poor cost control, or a business that must run at full throttle just to survive.

When a buyer sees that profitability disappears the moment volume dips or costs rise, they see risk. And once again, risk pushes valuation down.

Here’s where many owners get caught: they chase revenue because it feels like growth. They discount to win deals. They take on unprofitable customers “for the relationship.” They maintain outdated pricing while costs quietly rise. Over time, the business becomes addicted to volume instead of disciplined around value.

During due diligence, buyers will analyze not just your revenue, but your quality of earnings, your consistency, pricing power, and resilience. If your margins wobble year to year or barely hold together, they’ll either demand a lower price, insist on heavy contingency structures, or move on to a stronger, more stable acquisition.

The Fix: Start treating margins like a strategic priority, not an afterthought. Conduct a pricing review and ensure your rates reflect current costs, labor realities, and market positioning.

Identify unprofitable products, services, or customers, and either fix them or phase them out. Tighten operational efficiencies, reduce waste, and hold the team accountable to margin targets, not just top-line goals.

Strong, predictable margins tell buyers your business is disciplined, healthy, and capable of generating dependable returns. That confidence turns into higher offers, better deal terms, and protected value.

#6 Lack of Systems, Processes, and Documentation: When Success Depends on “How We’ve Always Done It”

One of the quietest yet most damaging value slashers is a business that runs on memory, habit, and tribal knowledge instead of documented systems. Many companies grow on grit, hustle, and experience, especially founder-led companies. That works… until it doesn’t.

From a buyer’s perspective, a business without standardized processes is unpredictable. It means performance relies on individual people, not proven systems. And anything that feels unpredictable lowers confidence, complicates transition, and potentially reduces value.

You’ll recognize this problem if any of these sounds familiar:

Employees train new hires by “shadowing.” Tasks are done based on “how Susan likes it done.” The answer to most operational questions starts with, “It depends…”

Procedures live in people’s heads instead of anywhere accessible. The business functions, but it does so informally. That might feel normal day to day, but to a buyer, it looks like a house held together by experience instead of structure.

If a key person leaves, or if the buyer takes over without your team’s full support, performance can drop quickly. That risk shows up as price reductions, extended earn-outs, and hesitation.

The Fix: Turn your business into a machine rather than a personality-driven operation. Start by documenting core processes: sales workflows, service delivery, customer onboarding, financial procedures, and daily operational routines. Create SOPs (standard operating procedures) that are clear, repeatable, and accessible. Introduce technology where it creates efficiency, consistency, and visibility. Build training systems that don’t depend on one person doing all the teaching.

When your business can show buyers well-documented workflows and predictable execution, it sends a powerful message: “This company doesn’t just operate, this company knows how it operates.” And that instantly increases trust, transferability, and value.

#7 No Strategic Positioning or Differentiation: When You Look Like Everyone Else When Selling Your Business

The final hidden value slasher is one many owners never notice because it hides in plain sight: lack of differentiation. If your business sounds like every other competitor in your industry standing out with “great service,” “quality work,” “competitive pricing”, then from a buyer’s perspective, you’re a commodity.

Commodities don’t command premium valuations. When there’s nothing distinct about your offering, brand position, expertise, market niche, or customer experience, buyers assume the only level your business truly competes on is price. That means thinner margins, less loyalty, and a business that’s easier for competitors to replicate, all of which drag value down.

Here’s the uncomfortable truth: if your business disappears tomorrow, and your customers could easily replace you with another provider without much disruption, then you don’t own a strong market position, you just occupy space in it.

Buyers want companies with an edge: a brand people recognize, a niche where they dominate, intellectual property or proprietary methods, a reputation that commands respect, or a clearly defined specialty that makes them harder to replace. When none of that is present, the business may operate fine, but it doesn’t stand out, and that shows up directly in valuation.

The Fix: Get intentional about positioning. Clarify what you do better than anyone else and lean into it.

Define your specialty. Strengthen your brand presence and reputation.

Become known for something specific rather than trying to be everything to everyone. Build credibility through testimonials, case studies, market authority, and consistent messaging. Explore ways to create defensibility, recurring revenue programs, proprietary processes, exclusive relationships, or specialized expertise.

When a buyer can clearly answer the question, “What makes this business different and hard to replace?”, your perceived value increases dramatically. And that’s when your business stops being just another option and starts being a premium acquisition.

Value Doesn’t Vanish Overnight, It Slips Away Quietly

The most dangerous part about these seven value slashers is that none of them feel urgent while you’re running the business. The doors are open, customers are happy enough, revenue is coming in, and operations mostly work. That’s why so many owners are blindsided later.

These issues don’t show up as emergencies; they show up as lost valuation, tougher negotiations, demanding buyers, drawn-out due diligence, or deals that collapse right when the finish line is in sight. Value isn’t lost in dramatic moments, it erodes slowly, through risks that feel manageable… until someone else is evaluating your company from the outside.

The good news is every single one of these problems is fixable with clarity, discipline, and intention. Strengthen leadership. Clean up financials. Reduce dependency on you, on a few employees, or a handful of customers.

Build processes. Define your positioning. Treat your business like the asset it truly is, not just something you operate day-to-day. Whether you plan to sell in two years, ten years, or never, addressing these value slashers will give you more options, more leverage, and a stronger, more resilient company.

The best time to prepare was years ago.

The second-best time is right now.

Read MoreIs Now a Good Time to Sell My Business? Why Timing the Market is a Bad Idea

If you’re a business owner thinking about selling, you’ve probably asked yourself: “Is now a good time to sell my business?” With headlines constantly shifting, interest rates rising, economic uncertainty looming, it’s easy to convince yourself to wait for “better” conditions. But here’s the reality: waiting for the perfect market often means waiting forever. Much like trying to time the stock market, trying to predict the exact right moment to sell your business is a gamble. And more often than not, it leads to missed opportunities, stalled plans, and lost value. Instead of obsessing over market conditions, the more important question is: Are YOU and your business ready to sell?

Why the Perfect Market Rarely Exists

The idea of a “perfect market” is more of a fantasy than a reliable benchmark. Markets are always in motion, shaped by global events, economic cycles, and investor sentiment. There will always be reasons to hesitate: inflation, interest rate hikes, geopolitical tensions, or even shifts in consumer behavior. Ironically, when the market feels perfect, it’s often already on the verge of changing. By the time most business owners recognize ideal conditions, they’re in the rearview mirror. Rather than trying to catch a fleeting peak, savvy sellers focus on factors within their control, like building a strong, transferable business and aligning the sale with personal and financial goals.

The Real Questions to Ask Instead

Instead of asking, “Is the market right?”, the better question is, “Am I ready?” Market conditions matter, but they’re only one piece of the puzzle. What truly drives a successful sale is the readiness of both you and your business. Are your financials clean and up to date? Have you documented your processes and reduced dependency on you as the owner? Do you know what your business is actually worth today? Most importantly, are you emotionally and financially prepared to move on? Buyers are looking for stable, well-run businesses, not perfect economic conditions. Focusing on your own readiness puts you in a position of strength, regardless of where the market stands.

A Real-World Example: The Cost of Waiting

Consider the story of a business owner who ran a successful restaurant in Texas. This owner decided to sell the restaurant at a higher price than what the market, and their strict time constraints, would realistically allow. Although they could have listed the business at an appropriate price point to meet these tight deadlines, they opted to set a premium asking price, hoping to secure the highest possible value regardless of the limited time available.

Normally, a seller has the option to wait for the highest offer, but in this case, time was a critical constraint from the start. Eventually, the owner began lowering the price to attract buyers within the limited timeframe, but these efforts came too late. Due to urgent family matters, the owner was ultimately forced to close the restaurant and focus on personal issues rather than continue operating while waiting for a sale. As a result, the owner lost the entire market value of the business and walked away empty-handed.

Focus on What You Can Control

While you can’t control interest rates, buyer sentiment, or the broader economy, you can control how prepared your business is for a sale. Focus on strengthening your operations, cleaning up your financials, and making your business less dependent on you personally. Document key processes, develop a strong management team, and ensure customer and vendor relationships are stable. These are the things that truly drive value in the eyes of a buyer, regardless of market conditions. A well-prepared business can attract strong offers in almost any environment, because buyers are ultimately looking for stability, scalability, and future potential, not just a good economy.

Conclusion: Timing the Market vs. Timing Your Life

At the end of the day, the perfect market is more myth than reality. Instead of trying to predict when the stars will align, focus on aligning the sale with your life and your readiness. When your business is solid, your financials are transparent, and you’re personally prepared to move on, you’re already in the best possible position to sell, regardless of outside market noise. Remember, successful exits aren’t about catching the perfect wave; they’re about building a business and a plan that buyers want today. So if you’ve been waiting for the “right time,” maybe that time is now.

Read More